Kehrer Group research has demonstrated that financial planning is a win-win-win for the advisor, the firm, and the financial institution, but bank and credit union-based advisors have been slow to embrace planning. When financial institutions and their investment services units want to encourage certain activities of client-facing personnel, a common practice is to set goals and/or provide financial incentives to, for example, sell more CDs or HELOCS (financial institutions) or do more advisory business or meet clients’ insurance needs (investment services). Naturally directors of financial institution-based advisors have tried this approach to encourage financial planning. Does it work?

For the answer we turned to Kehrer Group’s proprietary database of financial planning practices in 87 financial institutions to explore the link between goals and incentives and onboarding clients to the planning process.

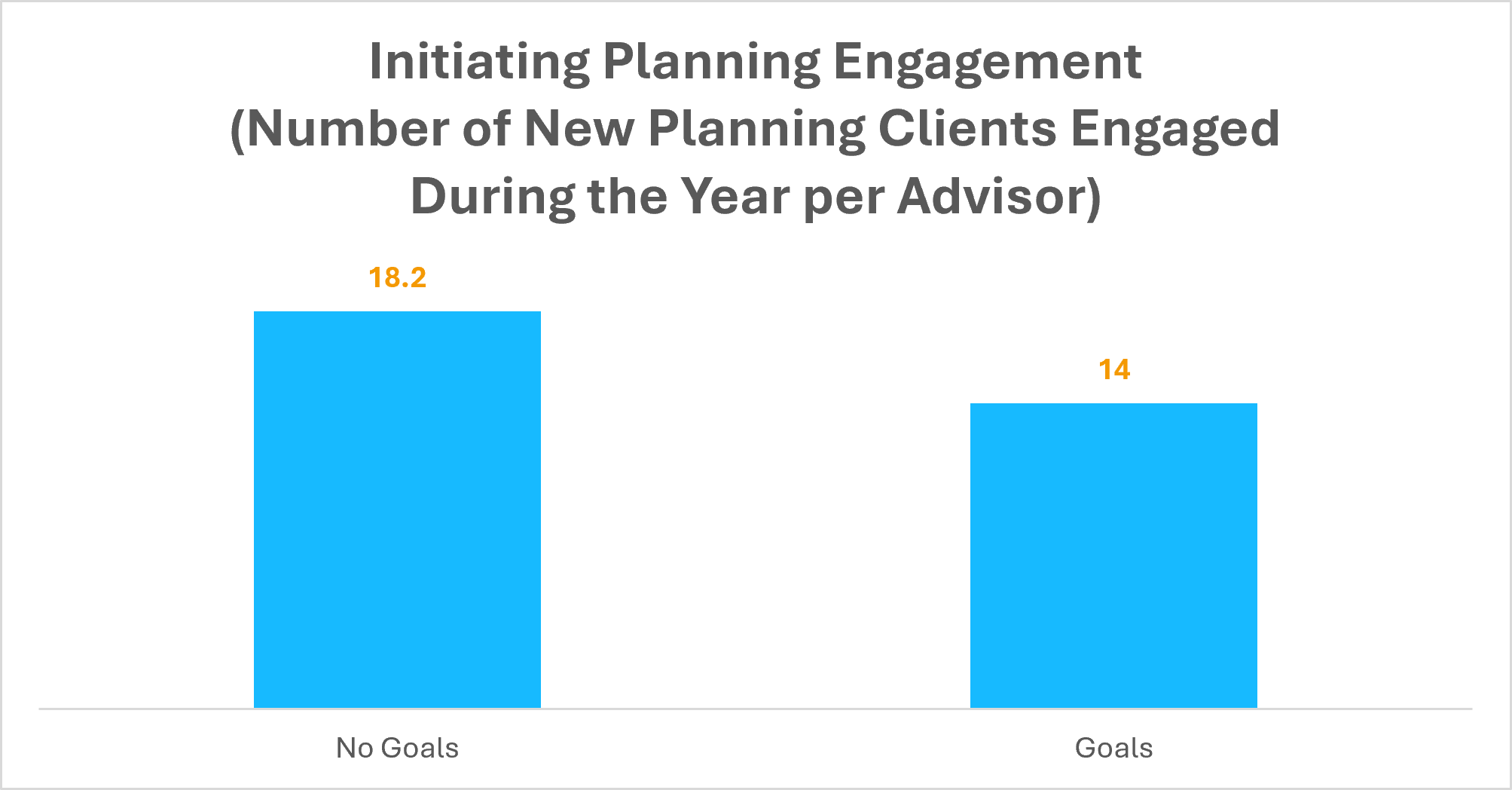

One-third of the firms in the database set financial planning goals for their advisors. But they actually have lower engagement rates for the number of new plans initiated or the share of clients onboarded to planning than firms that do not have planning goals.

Advisors in firms that do not set goals for financial planning initiate planning engagements with 18.2 clients a year, on average, 31% more than advisors who face planning goals.

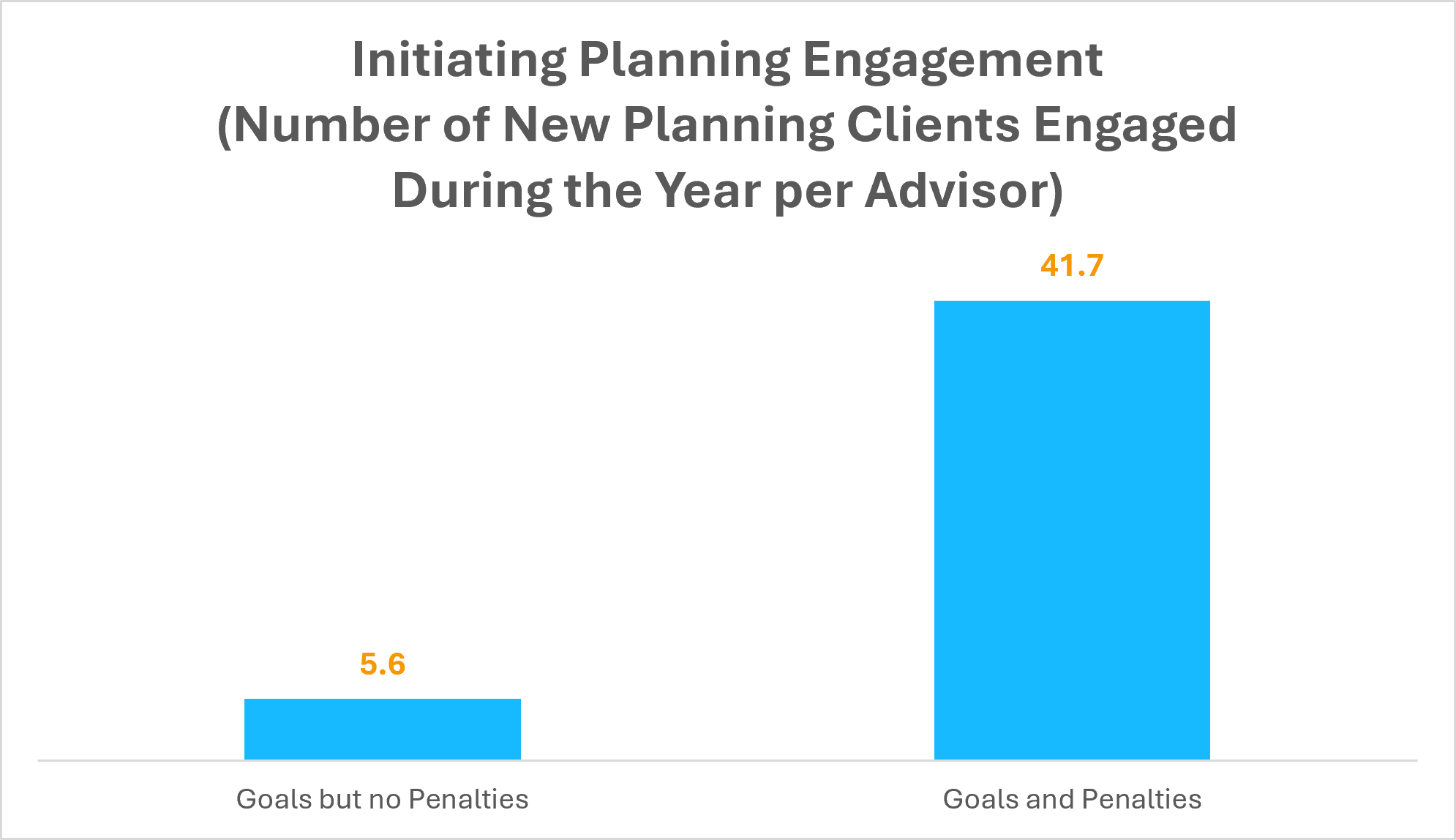

Part of the problem is that the goals are not enforced; only a quarter of the firms that set financial planning goals for advisors penalize them if they fall short. Advisors in firms that are penalized if they do not meet their planning goals average 41.7 new planning engagements a year, seven times the new plan productivity of advisors who are not penalized.

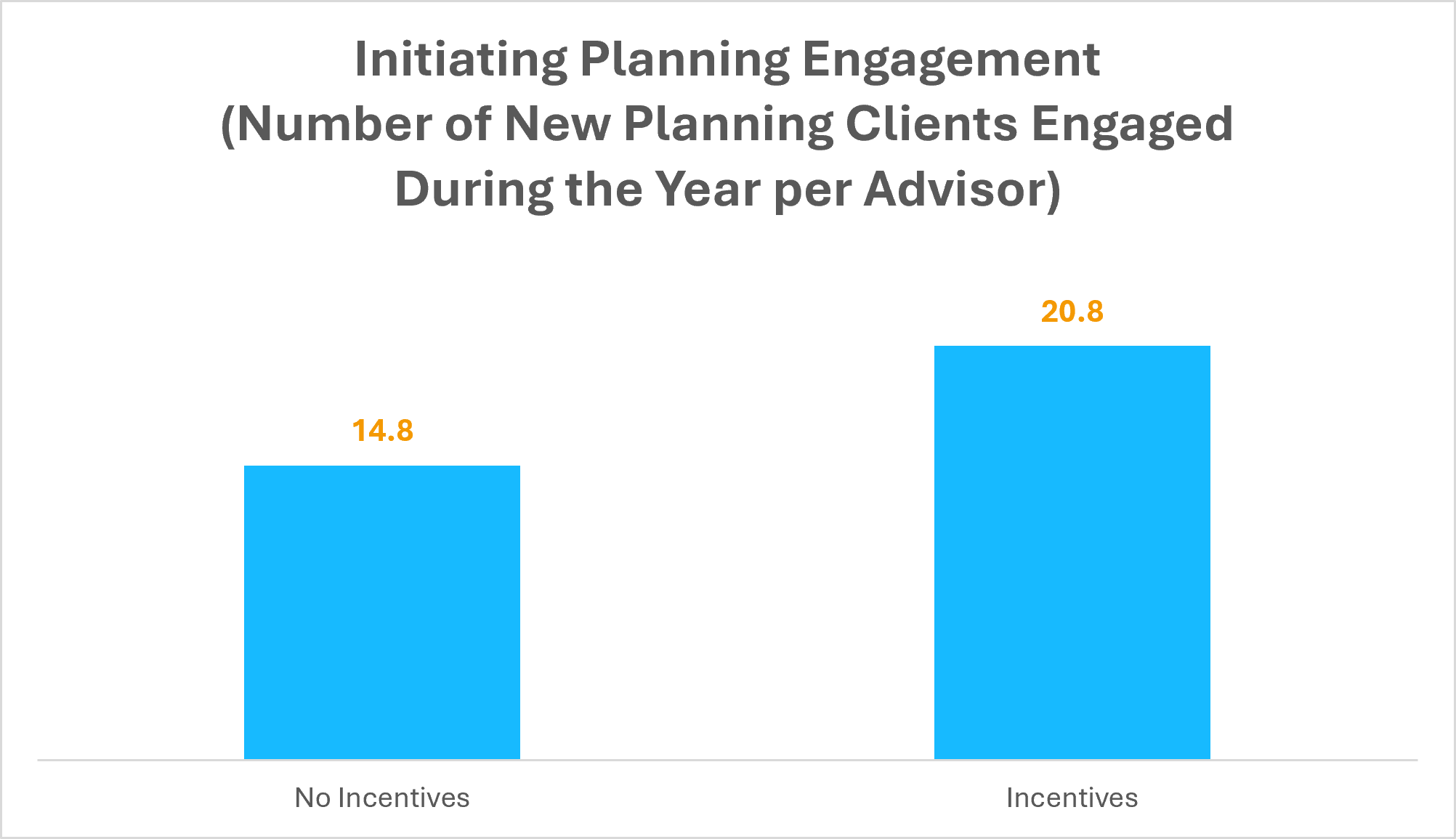

Fewer than one out of six of the firms in the database provide financial incentives for planning activity. Advisors in firms that earn additional compensation for their planning activity average 20.8 new planning engagements a year, 41% more than advisors in firms that do not compensate for planning activity.

As usual, financial advisors tend to do what they are paid to do. Why don’t all directors of financial institution-based advisors add rewards for financial planning activity to their advisors’ compensation plans? In part because some directors have found that too many advisors do the bare minimum to qualify for having worked on a plan, “checking the box” but arguably not engaging in the planning process. As some directors put it, “You pay for widgets, you get widgets.”

The question of whether financial incentives encourage advisors to embrace financial planning is bound up with issues like, “What is a quality financial plan? Who should have a financial plan? What is the appropriate type of planning for clients with different needs?” Once a director resolves these issues for the firm, the firm then has to review the plans to determine if they are up to muster. The typical sales manager in a bank or credit union manages around 20 advisors and probably can’t devote much time to reviewing their plans if each advisor is working on a few each week. Among the firms in the database, less than half do any kind of review of the advisors’ plans. In the firms that conduct reviews, advisors have three times the new planning engagement rate.

This analysis is part of a larger study by Kehrer Group sponsored by Raymond James Financial Institutions, “Win the Financial Planning Race: Best Practices in Driving Planning Engagement in Financial Institutions.” Other Highlighters in this series examine other levers in the Director’s toolkit, and their efficacy.

Executing on financial planning requires more than advisor intent – it requires scalable infrastructure. Raymond James supports financial institutions with integrated capabilities designed to address the operational, capacity and expertise constraints identified in the Kehrer research.

GOAL PLANNING & MONITORING. Scalable financial planning requires a consistent framework that advisors can apply across diverse client relationships. For banks and credit unions, Goal Planning & Monitoring provides a structured planning environment that can be scaled across an institution’s advisor force. This enables advisors to create, update and track client plans over time while reinforcing more consistent client engagement.

About Kehrer Group Highlighters

The Kehrer Group Highlighters package some of our most important findings, insights, and commentary into bite-size, digestible articles. We make the Highlighters available for free to the entire financial advice community—a small gesture of appreciation for a community that has done so much to support our work.

![]()

About Raymond James Financial Institutions

Advisors in the Raymond James Financial Institutions Division are generating, on average $890,000 in revenue, driven by the services that only a full-service broker-dealer can provide — including investment banking services, wealth and longevity planning, robust technology tools, curated advisor training, and a specialized financial institution support team — all of which help partners grow their investment programs, deepen relationships, integrate within the broader banking teams, and generate higher revenue per advisor.

![]()

About Kehrer Group

Kehrer Group is the bank and credit union financial advice community’s trusted partner for original thought leadership, insight based on data, and strategies that drive success. Kehrer Group’s legacy of research and analysis has advanced the delivery of investment services in banks and credit unions and shaped the industry into what it is today. Kehrer Group’s principals meld the wisdom gained from its long history in the industry with cutting-edge analytics, data that is robust and diverse, and a deep understanding of the key drivers of performance.

Learn more about what we do.